By Pete Pennicott | May 13, 2026

By Pete Pennicott | May 13, 2026

Yes, it is that exciting time of the year again. Treasurer Jim Chalmers has handed down the 2026-27 Federal Budget and as expected, this year’s announcement focused heavily on the Government’s tax reform agenda, with significant changes proposed for capital gains tax, negative gearing, and discretionary trusts.

For superannuation, the Budget proved to be a quiet night. Following the passage of the Division 296 tax measures and the soon-to-commence Payday Super reforms, the absence of further super changes provides welcome certainty and stability for the sector.

We have summarised the key measures most likely to affect you, your family, and your financial planning below. The full Budget details are available at budget.gov.au.

For our ongoing service package clients, your adviser will be in contact to provide guidance on the changes that may impact your strategy.

IMPORTANT: Please remember that unless specified, these measures are subject to becoming law, so confirm this before taking action.

From 1 July 2027, the 50% CGT discount will be replaced by cost base indexation for assets held longer than 12 months. In addition, a 30% minimum tax rate will apply to net capital gains.

These changes will apply to all CGT assets including property and shares held by individuals, trusts, and partnerships. They will also apply to pre-1985 CGT assets, which under current rules are exempt from CGT. Indexation will use the Consumer Price Index (CPI), similar to the rules that applied between 1985 and 1999, with ATO tools and guidance to support the calculations.

Transitional rules

For eligible CGT assets:

For pre-1985 (pre-CGT) assets, gains accrued before 1 July 2027 will continue to be exempt. Taxpayers will need to determine the value of a CGT asset as at 1 July 2027 as part of their tax return in the year the asset is sold. The ATO will provide tools to assist with this, either through a valuation or a specified apportionment formula.

Exemption for new housing

To support new housing supply, investors in new build residential properties will be able to choose either the existing 50% CGT discount, or the new cost base indexation and minimum tax.

A new build is broadly a dwelling constructed on vacant land, or where an existing property is demolished and replaced with a greater number of dwellings. Knock-down rebuilds or substantial renovations that don’t increase supply will not qualify. Subsequent purchasers cannot access the 50% discount.

Income support payment recipients, including Age Pension recipients, will be exempt from the new 30% minimum tax.

Superannuation funds not impacted

Importantly, these changes do not apply to superannuation funds, including SMSFs, which will continue to be eligible for the existing 1/3 CGT discount on assets held longer than 12 months.

The Government will limit negative gearing for residential property to new builds. From 1 July 2027, losses from established residential properties will only be deductible against rental income or capital gains from residential properties. Excess losses can be carried forward and offset against residential property income in future years.

Transitional rules

For established residential properties:

Exemptions

New builds can continue to be negatively geared before and after 1 July 2027. Properties held in widely held trusts (such as most managed investment trusts) and superannuation funds (including SMSFs) are also excluded. These changes apply to individuals, partnerships, companies, and most trusts. Other asset classes — such as shares and commercial property — are not affected.

The Government will introduce a 30% minimum tax rate on the taxable income of discretionary trusts. The tax will be paid by the trustee, who controls distributions. Beneficiaries (other than corporate beneficiaries) will receive a non-refundable tax credit for the tax paid by the trustee when they declare their trust income. Trustees will be required to calculate, report, and pay the minimum tax, and to notify beneficiaries of their entitlements.

To prevent franking credits being used to undermine the minimum tax, trustees that receive franked dividends will be required to apply their franking credits to pay the minimum tax. Corporate beneficiaries will not receive non-refundable credits for tax paid by the trustee.

Exemptions

The minimum tax will not apply to:

Some types of income will also be excluded, including primary production income, certain income relating to vulnerable minors, amounts to which non-resident withholding tax applies, and income from assets of discretionary testamentary trusts existing at announcement.

Rollover relief will be available for three years from 1 July 2027 to assist small businesses and others who wish to restructure out of discretionary trusts into another entity type, such as a company or a fixed trust.

A new permanent $250 Working Australians Tax Offset (WATO) will apply to income from work, such as wages, salaries, and the business income of sole traders. The WATO will apply automatically after you lodge your tax return, working in a similar way to the existing Low Income Tax Offset (LITO).

It is a non-refundable offset, meaning it can reduce tax payable (excluding the Medicare levy) to nil, but cannot result in a refund. The WATO will lift the effective tax-free threshold for income from work by close to $1,800.

From the 2026-27 income tax year, eligible Australian tax residents earning income from work will be able to claim an instant tax deduction of up to $1,000 for work-related expenses, without needing to itemise their claims or keep receipts.

If your work-related expenses exceed $1,000, you can continue to claim them in the usual way under existing rules (with appropriate records). Charitable donations, union and professional association fees, and other non-work-related deductions can still be claimed separately on top of the instant deduction.

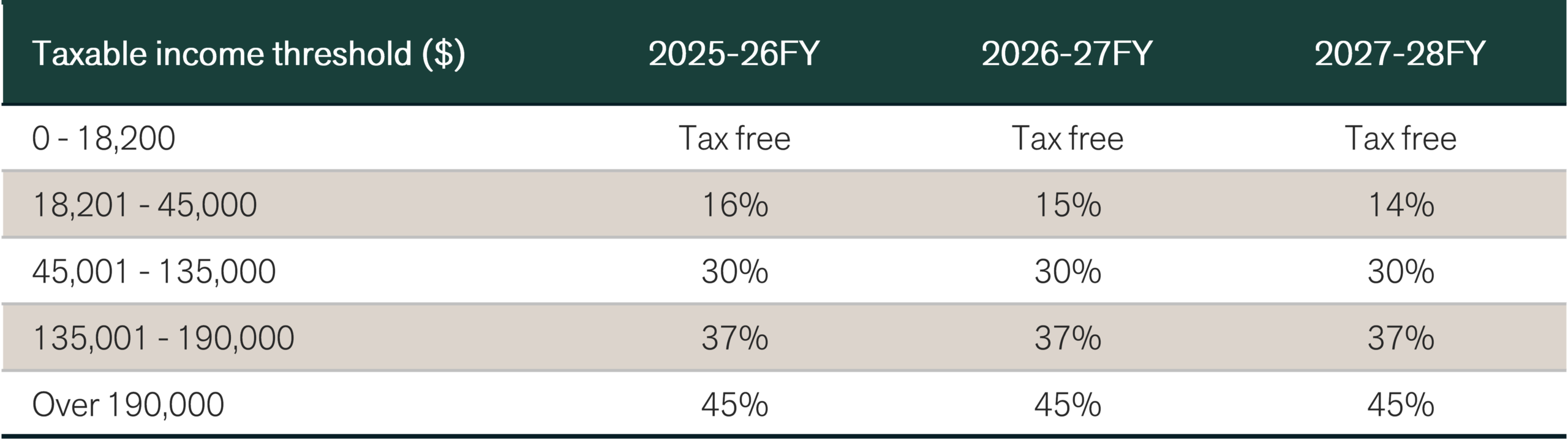

The previously legislated tax cuts will take effect as planned:

This provides a tax cut of up to $268 in 2026-27, and up to $536 from 2027-28.

The Government is adjusting the FBT treatment of electric cars. From 1 April 2029, a permanent 25% FBT discount will apply to all electric cars valued up to the fuel-efficient luxury car tax threshold (currently $91,387).

Transitional arrangements include: electric cars valued up to $75,000 provided before 1 April 2029 continue to receive the existing 100% FBT exemption; and electric cars above $75,000 (up to the luxury car threshold) provided between 1 April 2027 and 1 April 2029 will receive the 25% discount. Eligible vehicles will retain the discount rate that was in place when the arrangement commenced.

There were no new superannuation tax changes announced in this Budget. Three significant super reforms — already legislated — commence on 1 July 2026:

Payday Super

From 1 July 2026, employers will generally be required to pay Super Guarantee (SG) contributions at the same time as salary and wages, instead of quarterly. This is intended to make it easier for you to monitor your SG entitlements and reduce the incidence of unpaid super. The new rules also include changes to the earnings base for calculating SG and the SG charge, and changes to how the Maximum Contributions Base is applied.

Division 296

From 1 July 2026, an additional 15% tax will apply to the portion of earnings attributable to a Total Super Balance (TSB) above $3 million, with a further 10% (totalling 25% extra) on the portion attributable to a TSB over $10 million.

The tax is assessed to individuals (not the super fund), with impacted individuals having the choice to pay the tax personally or to elect for it to be released and paid from their super. To support the calculations, super funds will be required to calculate each member’s share of taxable earnings for Division 296 and report it to the ATO. First assessments will be issued after 30 June 2027 based on the 2026-27 income year. The rules will only tax realised capital gains accrued from 1 July 2026 onward.

Paid Parental Leave Super Expansion

Following the introduction of super on Commonwealth-funded Paid Parental Leave from 1 July 2025, Paid Parental Leave itself expands to six months from 1 July 2026. Eligible parents will receive super contributions over this longer period, helping reduce the long-term impact of career breaks on retirement savings.

The Government will permanently extend the $20,000 instant asset write-off for small businesses with turnover under $10 million. Assets valued at $20,000 or more can continue to be placed into the small business simplified depreciation pool. Provisions preventing small businesses from re-entering the simplified depreciation regime for five years after opting out will continue to be suspended until 30 June 2027.

For tax years commencing on or after 1 July 2026, companies with aggregated annual global turnover under $1 billion will be able to carry back a tax loss and offset it against tax paid up to two years earlier. Loss carry-back applies to revenue losses only and is limited by a company’s franking account balance.

From 1 July 2028, start-up companies with aggregated annual turnover under $10 million that generate a tax loss in their first two years of operation will be able to use the loss to generate a refundable tax offset, limited to the value of fringe benefits tax and withholding tax on Australian employee wages in the loss year.

The Government will amend eligibility for the Pension Supplement for recipients absent from Australia. The full rate of Pension Supplement will be extended from 6 weeks to 12 weeks for those temporarily absent from Australia, and will cease for those residing permanently overseas or temporarily absent for longer than 12 weeks. Under current rules, the Pension Supplement reduces to the basic amount after the first 6 weeks of a temporary absence.

Additional funding of $2.2 billion over five years has been allocated to improve service delivery, including funding for frontline staffing, enhanced safety at Services Australia centres, the Services Australia Cyber Security Uplift program, and improvements to the myGov platform.

The Budget includes several measures aimed at strengthening the aged care system.

Residential aged care supply

An additional 5,000 residential aged care beds per year will be funded, principally for those with limited financial means, supported through building subsidies and an increase to the Accommodation Supplement. Additional funding has also been provided for dementia care supports, including expansion of the Hospital to Aged Care Dementia Support program.

Improving access to home care

The Government will fully fund personal care services such as showering, dressing, and incontinence aids for all Support at Home recipients. Faster access to Support at Home places has also been announced, alongside improvements to assessments, hardship applications, and the end-of-life pathway.

Better care for older Australians

Additional funding has been provided for strengthened regulatory, governance, and quality arrangements, sector viability, and workforce supports.

The Government will remove the age-based uplift of the Private Health Insurance Rebate from 1 April 2027. Under current rules, older policyholders receive a higher rebate percentage than younger policyholders on the same income. For example, single people with income below $101,000 currently receive rebates of 24.188% (under 65), 28.139% (age 65-69), and 32.158% (age 70+).

From 1 April 2027, older policyholders will no longer receive this higher rebate. Savings will be reinvested in the aged care sector.

The Government will provide funding to extend the operation of the Consumer Data Right (CDR) and explore enabling taxpayers to share certain ATO-held data through it. The CDR currently allows individuals to share their banking and energy data with new providers to access better offers. Extending this to ATO data could potentially allow you to authorise the sharing of your tax-related data with your financial adviser, something the advice industry has long advocated for.

The Government will provide $17.8 million over four years to strengthen governance, supervision, and enforcement of managed investment schemes. Funding will support ASIC’s data capabilities in supervising the sector, strengthen governance requirements (in partnership with the Office of the Australian Auditing and Assurance Standards Board and Treasury), and consult on new data collection powers. ASIC will partially meet the cost through cost recovery.

The Government will provide $86.3 million over four years to deliver Phase 2 of the Counter Fraud Strategy, modernising the prevention and detection of fraud in the tax and super systems. This will enhance the ATO’s ability to detect and prevent fraud in real time, and expand live monitoring of fraudulent account access—including for high-risk superannuation changes.

The ATO will also be given new powers to pause the recovery of tax debts for taxpayers who are victims of fraud by tax intermediaries, and to waive those debts in appropriate circumstances. Existing garnishee powers will be expanded to include jointly held assets where such arrangements are being used to frustrate recovery actions.

If you have any questions or would like further clarification on any of the measures outlined in the 2026-27 Federal Budget, please feel free to book a chat with your adviser.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).