By Pete Pennicott | June 13, 2026

By Pete Pennicott | June 13, 2026

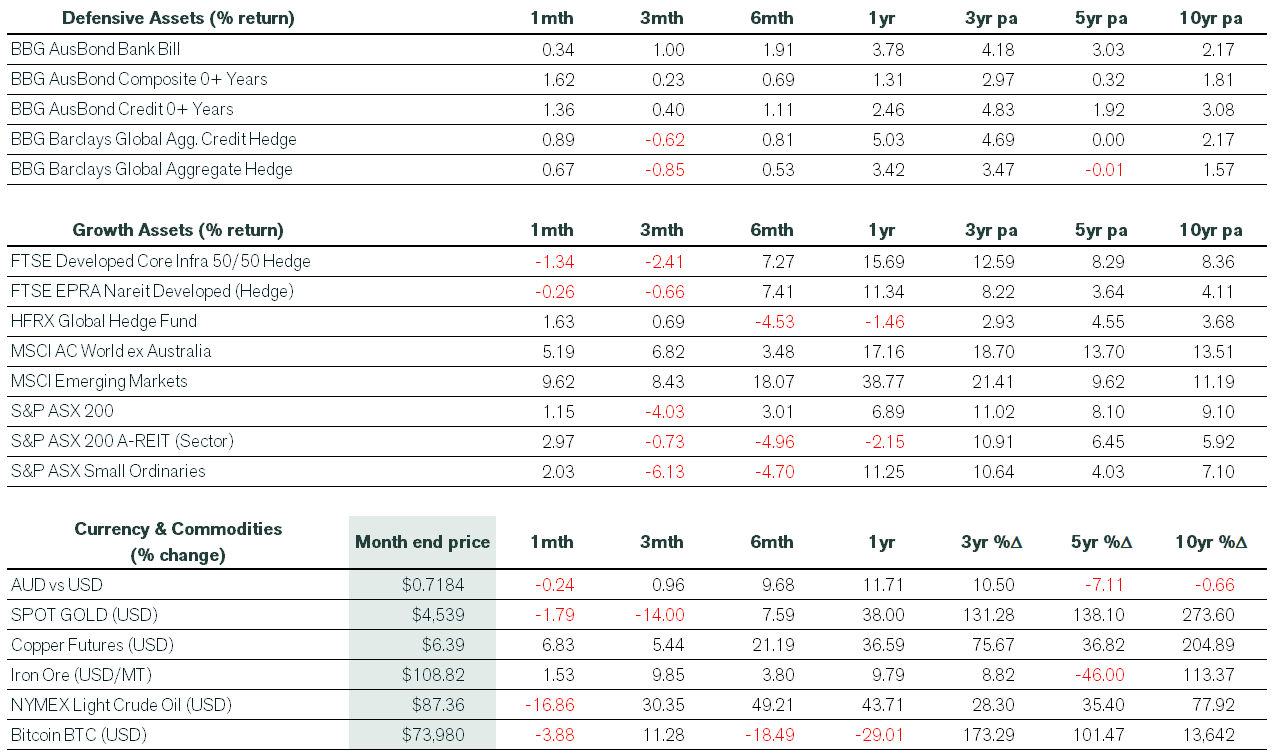

Global equities

US earnings have been the engine room of the rally. 84% of S&P 500 companies beat their profit forecasts for the first quarter, better than both the five and ten-year averages, which is rare air. From a sector perspective tech, communications and banks led the way. The sustained rally means that shares do not look cheap any more. The S&P 500 trades on a forward price-to-earnings ratio of 21.2x, well above its long-run average.

International shares delivered another strong month. The MSCI All Country World Index rose 5.4% in local currency terms and 5.1% unhedged. Contributions were spread across regions, but the US led on the back of tech and AI stocks. Europe and Japan also gained as investors looked beyond Wall Street. The standout was emerging markets, up 9.6% in Australian dollar terms. Korea and Taiwan drove the gains thanks to their semiconductor industries. China was the exception, falling for the month.

Real assets were mixed in May. Global listed property declined 0.6% after April’s strong gains, despite steadier bond yields late in the month. Infrastructure also weakened as investors favoured higher-growth sectors and reduced exposure to more defensive assets following the strong recovery seen in previous months.

Australian equities

Australian shares delivered positive returns but lagged major offshore markets, with the ASX 200 rising 1.1%. The performance gap between sectors was huge. Materials led gains, up 10.5%, as copper and iron ore prices rose on expectations of stronger demand from AI infrastructure and electrification trends. Consumer discretionary and real estate also benefited from improving investor sentiment. At the other end, healthcare (-9.2%), utilities (-7.6%), energy (-5.9%) and communication services (-4.2%) were the weakest sectors. Smaller companies outperformed larger peers, with the ASX Small Ordinaries gaining 2.0%.

Fixed interest, currencies & crypto

Fixed interest markets delivered positive returns in May as bond yields eased from their intra-month highs. Australian fixed interest performed particularly well, with the Bloomberg AusBond Composite 0+ Yr Index rising 1.6%, as softer inflation data and weaker labour market conditions led investors to scale back expectations for further interest rate increases. The Australian 10-year yield ended the month 23 basis points lower at 4.84%, after coming close to its year-to-date high of 5.11% mid-month. Global fixed interest also advanced, with the Bloomberg Global Aggregate (hedged) returning 0.7%, while credit markets edged higher on tighter global spreads.

Oil was the big story elsewhere. Brent crude fell 27% over the month to US$91 a barrel as a Middle East ceasefire raised hopes that the Strait of would reopen. While markets are optimistic, the situation remains fragile and the risk premium in oil prices has reset higher, limiting further declines.

Source: J.P. Morgan Asset Management.

Gold was volatile, trading between US$4,372 and US$4,550 an ounce. The US dollar strengthened, while the Australian dollar dipped during the worst of the conflict-related nerves but recovered to around 72c by month-end, close to long-term purchasing power parity.

Australia

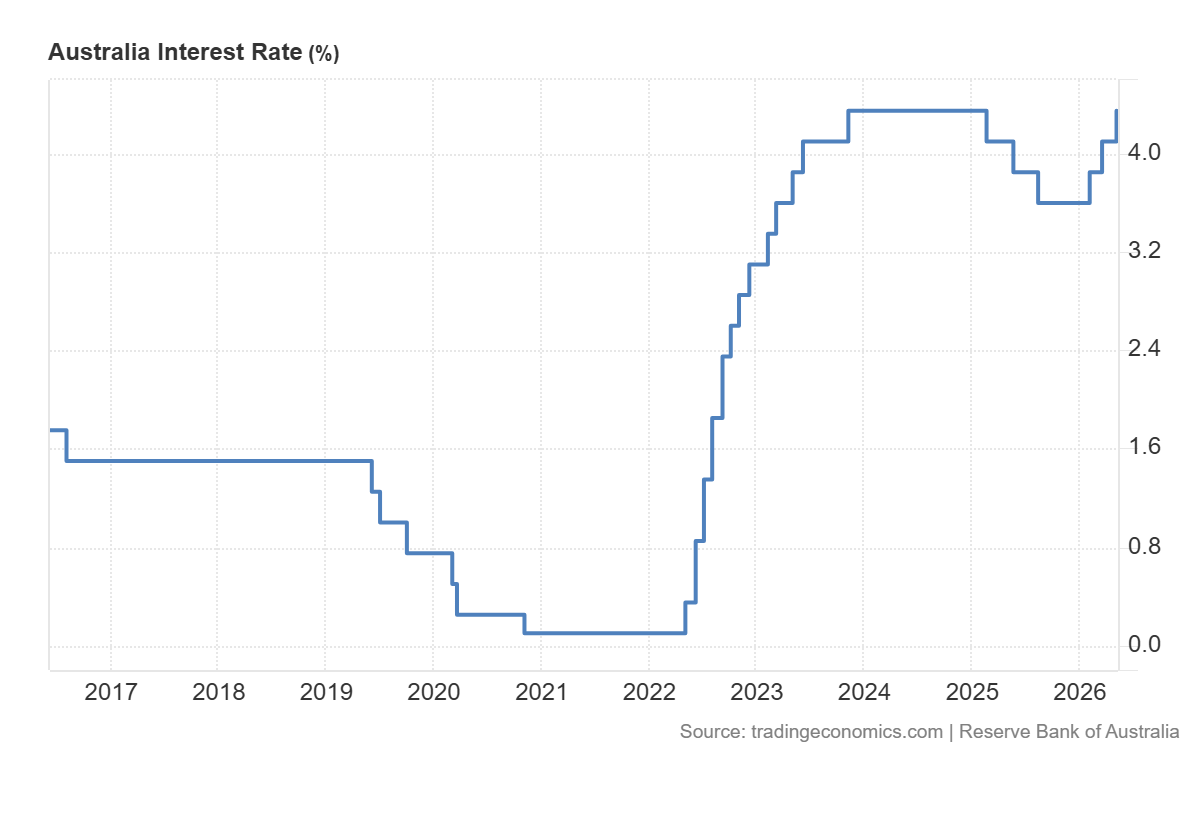

At its May board meeting and for the third meeting in a row, the RBA increased rates. The 25 basis point rate hike took the official cash rate to 4.35% in a definitive 8-to-1 vote. The move fully unwinds last year’s easing cycle and the cash rate is now back to its post-pandemic peak.

There was some better news on inflation. April’s monthly CPI came in at 4.2% year-on-year, which is higher than the RBA target band, but lower than economists expected. Core inflation (which strips out volatile items like fuel and fresh food) was 3.4%. As a result, market now pricing in less than one more rate hike (22 basis points) by the end of 2026.

The jobs market is starting to soften. Unemployment rose to 4.5% in April and overall employment fell by 18,000, with both full-time and part-time jobs declining. By historical standards 4.5% is still low, and the participation remains high, so there’s no reason to panic yet. Household spending fell 1.1% in April, which is a sizeable. Higher interest rates, sticky inflation and weak wage growth are all weighing on consumers. Business confidence is also subdued, with businesses reporting that input costs are rising faster than what they can charge customers and squeezing their profit margins.

The 2026 Federal Budget added another wrinkle. Tax reforms around negative gearing and capital gains tax will make property investing less attractive, slowing new lending to investors. That means slower credit growth, which is a key driver of bank profits – part of why bank shares have come under pressure. Housing activity has also softened, with falling auction clearance rates and weaker buyer sentiment.

United States

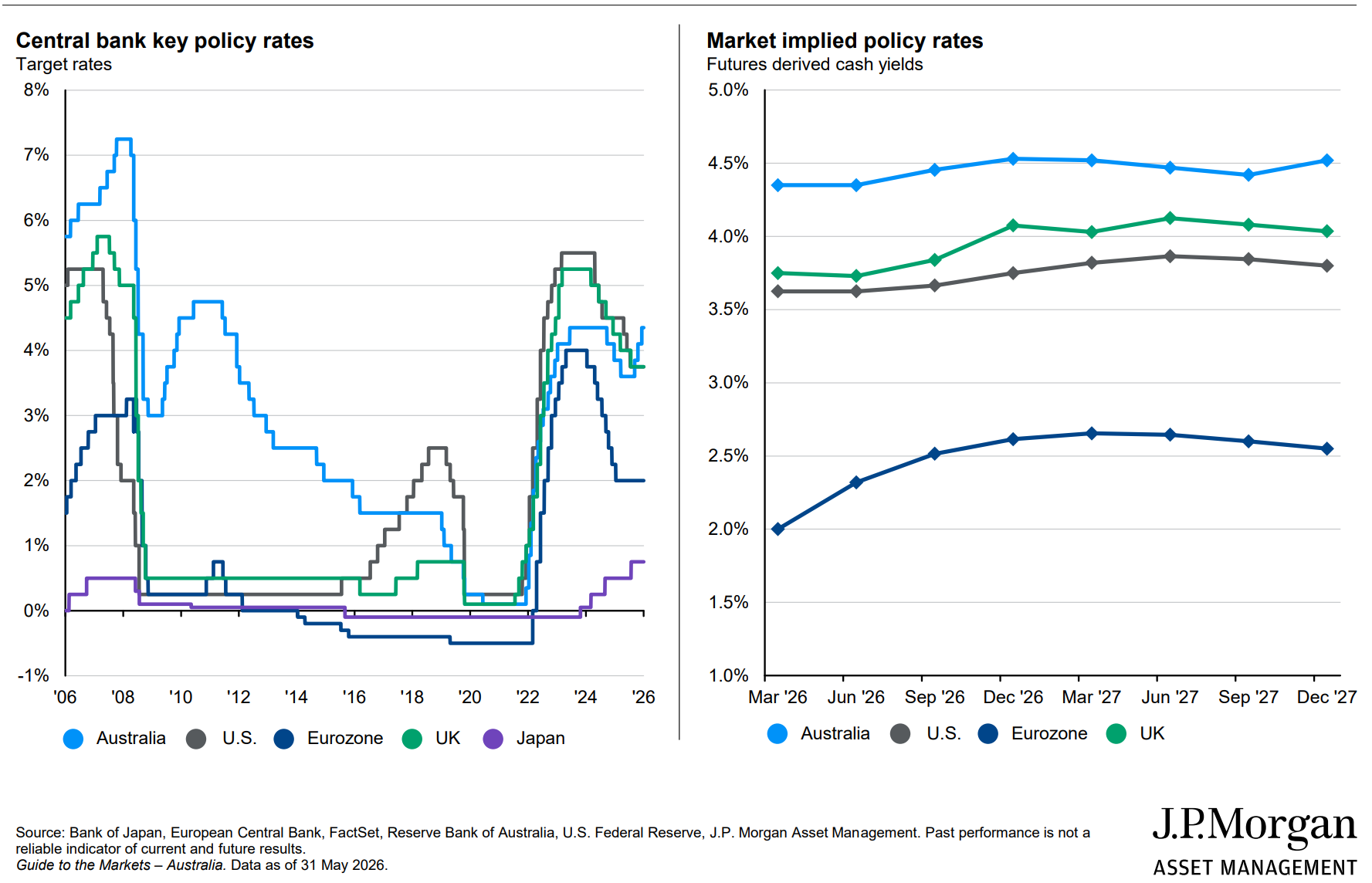

US economic data keeps surprising on the upside, and the world’s largest economy has felt the Middle East conflict less than most others. The unemployment rate ticked down 0.1 percentage points to 4.3% in April, and wages grew 3.6% over the year —both healthy figures. Tighter immigration policy means the labour force is growing more slowly, so fewer new jobs are needed each month to keep unemployment steady.

Looking ahead, Trump administration’s “One Big Beautiful Bill” is also expected to add roughly 1% of GDP in fiscal stimulus this year, providing a meaningful tailwind.

It isn’t a perfect picture however, and inflation is the catch. The core PCE deflator (the Federal Reserve’s preferred inflation measure) ran at 3.3% over the year to April, and 3.8% on a six-month annualised basis. Both are well above the Fed’s 2% target. Money markets now expect one 25bp hike from the Fed within a year, rather than the cut they had been pricing a month ago.

There has been a sell-off in US bonds in recent months, and the US 10-year Treasury yield has risen about 50 basis points since early March to sit around 4.5%. Part of that move is the change in rate expectations, but investors are also demanding more compensation for inflation risk and for the US government’s rising debt levels. New Fed Chair Kevin Warsh takes the chair at the June meeting and markets will be watching closely to see how he handles the tension between above-target inflation and a slowly cooling economy.

Rest of the world

Around the world, there is an expectation that inflation rates peak around the middle of the year and remain above central bank targets. This should lead to a tightening cycle response that is likely to vary materially across markets.

The European Central Bank is preparing for a hike at its June meeting after Eurozone inflation surged in April, while the Bank of Japan continues its gradual normalisation. UK 30-year Gilt yields touched 5.15% during May and 30-year Japanese government bond yields hit a record high of 4.13%, before easing back as rate-hike expectations were priced out and oil prices retreated.

Global manufacturing surveys remained in expansion territory, with India a continued standout. The wider takeaway from May: AI investment and resilient consumer spending are still driving share markets higher, even as bond markets warn that inflation and government debt risks haven’t gone away.

How can we help?

Appreciate you taking the time to read, and ff you want to discuss any of the above information or your personal investment strategy, then book a chat with your financial adviser here.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).