By Pete Pennicott | April 10, 2026

By Pete Pennicott | April 10, 2026

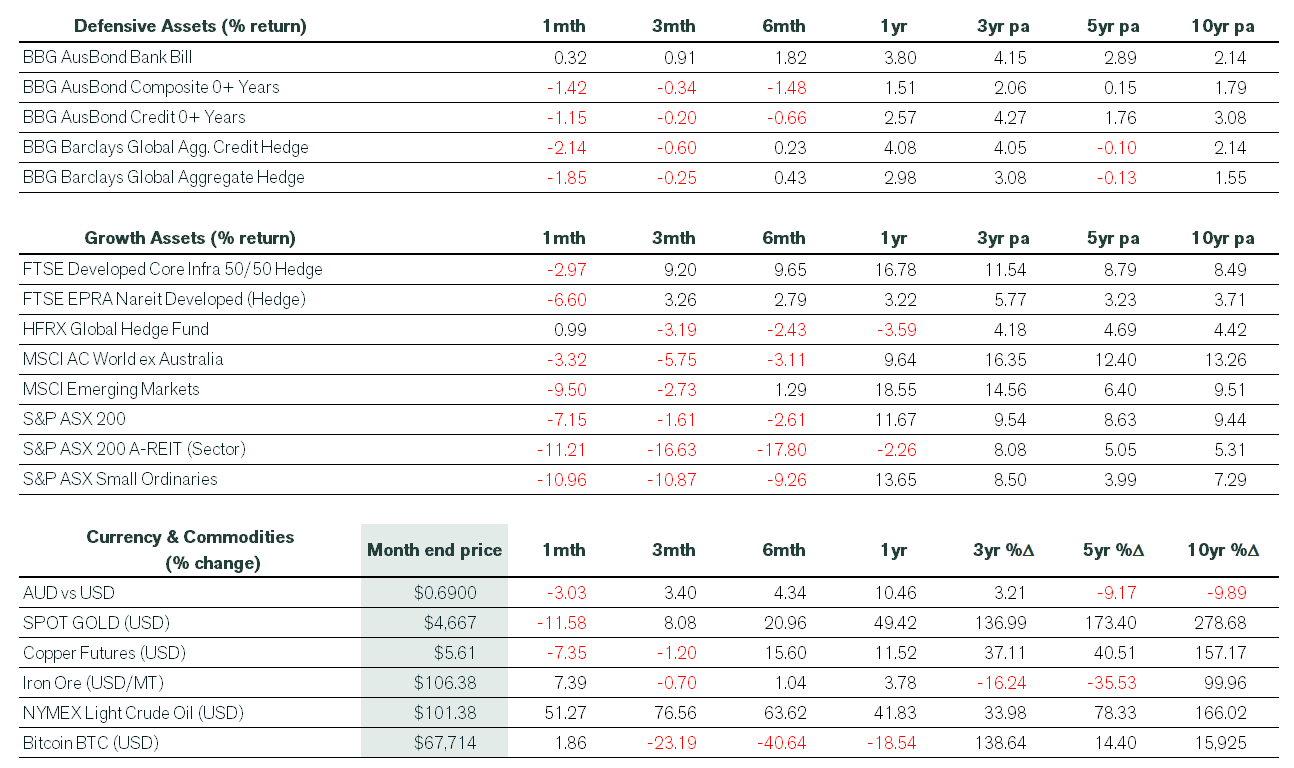

Financial markets were rocked in March by the war in Iran and the closure of the Strait of Hormuz, which sent oil prices surging and stoked widespread fears of stagflation. Volatility returned with force as risk assets sold off sharply, the US dollar strengthened and Treasury yields rose across the globe. Credit spreads widened as investors repriced risk throughout the month.

The US Federal Reserve held the funds rate unchanged at 3.5%–3.75% at its March policy meeting. In contrast, a divided RBA lifted the cash rate by 25bp to 4.10% in a 5–4 decision its second increase for the year, effectively reversing two of last year’s three rate cuts.

Global equities

A severe oil price shock saw global equity markets slump in March, with the MSCI ACWI ex-Australian index down 6.2% when measured in local currency terms. However, the depreciation of the Australian dollar throughout the month buffered losses for unhedged domestic investors (-3.3%). Losses were more pronounced in emerging market equities, where a resurgent US dollar and an abrupt loss of risk appetite sliced around 10% off returns (-10.5% in local currency and -9.5% in Australian dollar terms).

Diversification provided little benefit to investors during March, as asset correlations increased on heightened risks of stagflation — a scenario of economic stagnation and high inflation that has historically proven exceptionally challenging for policymakers and markets alike. Growth and value indices both posted steep losses, but small caps saw some of the biggest falls as investors sought insulation from macro risks and geopolitical events.

Including dividends, the benchmark S&P 500 index declined 5.0%, the tech-heavy Nasdaq 100 lost 4.8%, and the Dow Jones Industrial index fell 5.2%. The Magnificent Seven declined 5.6%, with losses deepest among small cap growth stocks.

Australian equities

At home, the ASX 200 lost 7.2%, led lower by the resources and technology sectors. The Small Ords fell 11.0%, while A-REITs slumped 11.2% as rising discount rates weighed heavily on valuations. Global property fell 6.6%, with listed infrastructure posting a more muted decline of 3.0%.

Sector performance for March was almost entirely negative, with Energy (+20.4%) and Utilities (+4.9%) the standout performers, and Consumer Staples (+1.7%) the only other GICS sector to deliver a positive total return. At the other end of the spectrum, Materials (-13.0%) fell hardest, closely followed by Information Technology (-12.5%).

Fixed interest, currencies, commodities, crypto

Fixed interest markets failed to provide a safe haven as inflation risks rose on the back of higher oil prices. The Australian composite bond index fell 1.4%, while the global aggregate bond index lost 1.9%. Cash proved to be the month’s shining light, with bills delivering a positive 0.32%.

Gold lost its glitter in March, with the US dollar spot price declining 11.6%. The sharp change in trajectory was likely driven by investors seeking liquidity as risk was taken off the table — the ASX gold sub-sector slumped more than 20% over the month, leaving it down 11% year to date.

In stark contrast, crude oil prices jumped over 50% in March. Brent Crude (+63%), the benchmark for two-thirds of globally traded crude, posted its strongest monthly rise since the 1970s. Prices briefly came within reach of US$120 a barrel, with downstream effects flowing through to Australian petrol prices amid signs of panic buying and reports of supply shortages at some service stations.

Australia

Australia’s GDP grew 0.8% quarter-on-quarter and 2.6% year-on-year for the December quarter, well ahead of consensus expectations. While consumer spending was relatively subdued, government spending jumped 0.9% over the quarter. Since mid-2022, public sector spending has been a key driver of output growth while also contributing to elevated inflation and eroding household purchasing power. At year end, the household saving ratio climbed to 6.9% from 6.1%, its highest level since September 2022 suggesting households may be banking income gains rather than lifting discretionary spending, as expectations of higher interest rates in 2026 continue to mount.

A surge in part-time jobs lifted domestic employment by 48,900 in February, following a gain of 17,800 in January. However, the headline unemployment rate rose to 4.3% from 4.1%, as workforce participation increased. Meanwhile, the February CPI inched down to 3.7%, and trimmed mean inflation printed at 3.3%. The monthly inflation report was released after the RBA had already pulled the trigger on a 25bp rate hike at its March meeting, its second increase for the year.

United States

In the US, core inflation cooled in February, with the CPI ex-food and energy rising 0.2% month-on-month and 2.5% year-on-year — the slowest annual rise since March 2021. Lower prices for used cars and motor vehicle insurance helped offset higher costs for gasoline and groceries. The pullback in underlying inflation also reflected lower housing costs, with rent of primary residence rising just 0.1%, the least in five years. Including food and energy, headline CPI advanced 0.3% month-on-month and 2.4% year-on-year.

The Federal Reserve held US interest rates steady at its March meeting. The Fed’s quarterly summary of economic projections pointed to higher inflation, steady unemployment and a single rate cut for 2026, as officials assessed the unfolding conflict in the Middle East. Chairman Powell noted that rising oil prices would push up inflation, but that the duration and scope of that upward pressure remained unknown. He also signalled that the Fed would typically look through the inflationary effects of a short-term energy supply shock when determining the path for rates, a nuanced message that markets will be watching closely in the months ahead.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).