By Pete Pennicott | March 19, 2022

By Pete Pennicott | March 19, 2022

A Bill implementing the Government’s key 2021-22 Federal Budget super changes recently passed parliament and received Royal Assent.

Outlined below is a brief explanation of some of the key changes and how you could benefit.

Whether you’re thinking about retirement, have already retired, or even looking to purchase your first home, there is likely to be value in reviewing your circumstances and understanding how these super changes could benefit you.

If you are unsure or want to chat about how these superannuation changes impact you, please make time to chat with your adviser.

Individuals aged 67-74 will have increased opportunity to contribute to super with the following changes:

Currently, the work test requires you to undertake work for at least 40 hours in a consecutive 30 day period in the financial year a super contribution is made. Alternatively, you may be eligible to apply the work test exemption.

This requirement is removed from 1 July 2022 for individuals aged 67-74 if making personal after-tax contributions and salary sacrifice contributions. The removal of the work test may make it easier for you to make contributions.

It is important to note that the work test (or work test exemption) still applies if you make a personal contribution and wish to claim a tax deduction.

Other eligibility requirements to make contributions continue to apply, such as total super balance limits and contribution caps. See ato.gov.au for more details.

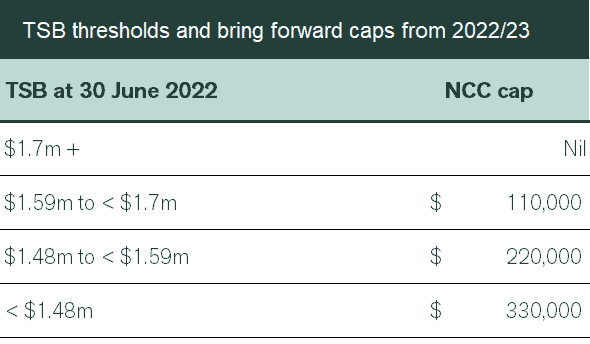

Caps apply to limit the total contributions that you can make to super. The current annual non-concessional contributions (NCC) cap is $110,000. NCCs include:

If you meet certain requirements, you may be eligible to ‘bring-forward’ NCCs from future financial years to make even larger contributions. This is known as the ‘bring-forward rule’. If you’re eligible, you may be able to contribute up to $330,000 either in a single financial year, or over a three year period.

Currently, you need to be less than 67 on 1 July of a financial year to be eligible to use the bring-forward rule. From 1 July 2022, you may be able to access the bring-forward rule if you’re aged less than 75 on the prior 1 July. Other eligibility rules will continue to apply, such as the total super balance limits.

The following table summaries the maximum NCCs that can be contributed in 2022/23 based on your total super balance as at 30 June 2022:

NOTE: Contribution caps apply to both concessional and non-concessional contributions. Care should be taken to avoid breaching your cap as additional tax and penalties may apply. For further information visit ato.gov.au or get in touch with us.

Downsizer contributions allow eligible individuals to contribute some or all of the proceeds of the sale of their home, without impacting other contribution caps. Unlike NCCs, downsizer contributions do not have a total super balance limit, or an upper age limit. This means it could be a great, final way to boost super for those who don’t meet other eligibility rules to contribute, or where the NCC cap has been earmarked for other purposes.

From 1 July 2022, the eligibility age is reducing from 65 to 60. The age reduction increases the number of individuals who may be eligible to make a downsizer contribution and boost their retirement savings.

Provided certain other conditions are met, it may be possible to contribute up to $300,000 per person (or $600,000 per couple) from the proceeds of selling your home.

Downsizer contributions won’t count towards your concessional or non-concessional contribution caps.

You’ll need to make the contribution within 90 days of settlement of your sale, and you need to complete the required forms to notify your fund that you’re making a downsizer contribution, no later than the time your contribution is made. You must have reached the eligibility age at the time of contributing.

Aside from super being a concessionally taxed investment, there are a number of other ways a downsizer contribution could benefit you.

Funds in super accumulation phase are an exempt asset for social security purposes while you are under your Age Pension age. This could help increase or maintain your or your spouse’s entitlement to a pension or other benefit. Also, making a downsizer contribution together with an NCC could help you contribute even more of your home sale proceeds into the concessionally taxed super environment.

Other eligibility rules and requirements apply. Before you contribute it is important to seek advice and if you are unsure then please get in touch with us.

The First Home Super Saver Scheme (FHSSS) allows you to make voluntary contributions of up to $15,000 per year within your concessional and NCC caps and you can later withdraw an amount of those voluntary contributions plus earnings (calculated at a set rate by the ATO on the amount you withdraw.

The maximum amount of voluntary contributions that you can withdraw increases from $30,000 to $50,000 from 1 July 2022. This boosts the amount that can be accessed from super and directed to buying your first home.

As the scheme allows the withdrawal of voluntary contributions, consideration must be given to not only whether using super is the right approach for you but the type of contribution you will make. For example, salary sacrifice amounts (if an employee), personal deductible contributions or non-concessional (after-tax) contributions).

There is a range of criteria to withdraw your super under this scheme as well as ensuring the funds are used to purchase your first home which is outlined on the ATO website.

Superannuation Guarantee (SG) requires employer to pay a minimum level of super support for eligible employees. One criteria for an employee to be eligible is based on that employee’s monthly earnings being at least $450 per month. However, this threshold is abolished from 1 July 2022.

allowing all eligible employees to receive SG paid into their super fund.

This measure primarily assists low-income earners to have employer contributions paid to super boosting their retirement savings. SG contributions count towards your concessional contribution cap and should be taken into consideration when determining any other contributions made.

Business owners should review their processes to ensure that SG is paid for all eligible employees. Penalties may apply if SG is unpaid or paid late.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).