By Pete Pennicott | March 10, 2026

By Pete Pennicott | March 10, 2026

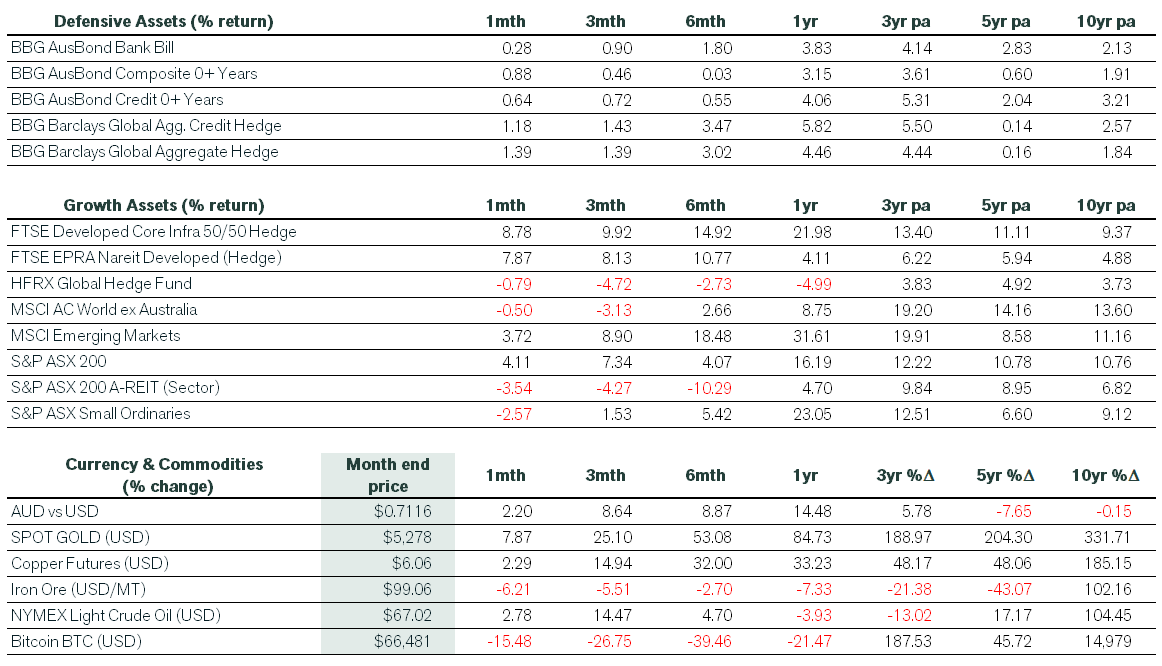

Further strength in the Australian dollar throughout February continued to impact global returns for unhedged domestic investors, while the ASX 200 moved higher on positive interim earnings reports. The key domestic economic news during the month was the RBA hiking the cash rate by 25bp to 3.85% and forecasting that inflation would not return to its target range anytime soon. Governor Michele Bullock said the three rate cuts in 2025 had “obviously given much more impetus” than expected and noted “…the housing market’s been a big part of that.”

In the US, the Supreme Court rejected Trump’s Liberation Day tariffs in a 6-3 ruling. Trump had invoked the International Emergency Economic Powers Act (IEEPA) to justify his tariffs. Following the shock ruling, Trump announced tariffs would instead be lifted “to the fully allowed, and legally tested, 15 per cent level.”

Global equities

Global equity markets moved higher in February when measured in local currency terms, with the MSCI ACWI ex-Australian index up 1.4%. However, the appreciation of the Australian dollar throughout the month saw returns for unhedged domestic investors in negative territory (-0.5%). It was a similar theme for emerging market equities, where the weak US dollar and a global cyclical upswing added to the recent rally (+5.0% in local currency and +3.7% in Australian dollar terms).

There was mixed performance across US indices as fierce sector rotation continued away from the Magnificent Seven (-7.3%), which experienced its worst decline since March 2025. Equal-weight, mid-cap and value exposures outperformed, while mega-cap tech, growth and AI-threatened software companies weighed on index returns. Including dividends, the benchmark S&P 500 index declined 0.8%, the tech-heavy Nasdaq 100 lost 2.3%, while the Dow Jones Industrial index returned 0.3%. In contrast, the S&P MidCap 400 returned 4.1%.

Australian equities

At home, the ASX 200 gained 4.1%, as large caps posted strong interim earnings results, capping a volatile but overall positive reporting season. The index closed the month at above 9,000 for the first time and recorded its third consecutive monthly gain. Big moves during February were seen in the major banks, led by CBA (+18.5%) and NAB (+13.0%). BHP (+15.5%) also had a stellar month, while many healthcare and tech names saw steep negative returns. Notably, only 26 ASX 100 stocks outperformed the index. CSL (-19.1%) was the worst performer among the blue-chip names and has lost over 40% over the last twelve months.

Fixed interest, currencies, commodities, crypto

Fixed interest markets had a solid month, as investors became increasingly nervous about geopolitical risks. This was also reflected in stronger gold and energy prices, however the so-called “crypto winter” continued, with Bitcoin slumping a further 15%.

The collapse of UK mortgage firm Market Financial Solutions (MFS) saw banks and listed private credit companies sell off. There are fears that fraud may be to blame for the £930m (A$1.8b) shortfall in collateral backing of MFS-originated loans. The shock permeated public markets with the KBW Nasdaq Bank Index slumping 4.9% on the final day’s trade for February. By month’s end, a group of six alternative asset companies that includes sector giants Apollo, KKR and Blue Owl, saw an average drawdown of 43% from their all-time highs.

Australia

On the economic front, ANZ job ads recorded their strongest monthly rise in nearly three years in January, pointing to a short-term lift in labour demand at the start of 2026. Later in February, the ABS revealed that the trend unemployment rate had decreased to 4.1% in January and trend employment growth was close to 25,000 a month. Meanwhile, the RBA lifted the cash rate to 3.85%, reversing one of last year’s three 25bp rate cuts. Despite weak wages growth over the last twelve months, inflation has become further entrenched and more broadly based. Poor productivity growth and capacity constraints are being tested by strong domestic spending across the private and public sector. This sees markets now positioned for another two rate hikes in 2026.

United States

In the US, retail sales were flat in December and had declined slightly over the prior year when adjusted for inflation. Households scaled back spending on motor vehicles and other big-ticket items, but it was unclear how much of this was due to new seasonality around Black Friday sales, a fatigued consumer, the effects of the government shutdown, or stalled population growth. Similar to Australia, wage growth continued to slow, but in stark contrast, productivity growth is booming (with the effects of AI yet to be felt). Meanwhile, US job growth unexpectedly accelerated in January (+130,000) and the unemployment rate fell to 4.3%. The job gains were well above the monthly average of 33,000 in 2025, and reinforced market expectations of no further cuts to the funds rate in the very near term.

Rest of the world

Elsewhere, the UK economy expanded by 1% in the December quarter, led by the services and production sectors. For 2025 as a whole, the economy expanded by 1.3%. Euro zone industrial production declined 1.4% in December on lower output of capital goods, marking the steepest monthly contraction since April 2025. In emerging markets, India’s annual inflation accelerated to 2.75% in January, which remains within the Reserve Bank of India’s band of 2%–6%. The saw the RBI keep its key repo rate at 5.25% during its February meeting, after cutting it by 25bp in December, amid confidence in a softer inflation outlook. Finally, China’s new home prices across 70 cities fell 3.1% over the year to January. It is the 31st straight month of contraction and the sharpest drop since June 2025.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).