By Pete Pennicott | January 12, 2024

By Pete Pennicott | January 12, 2024

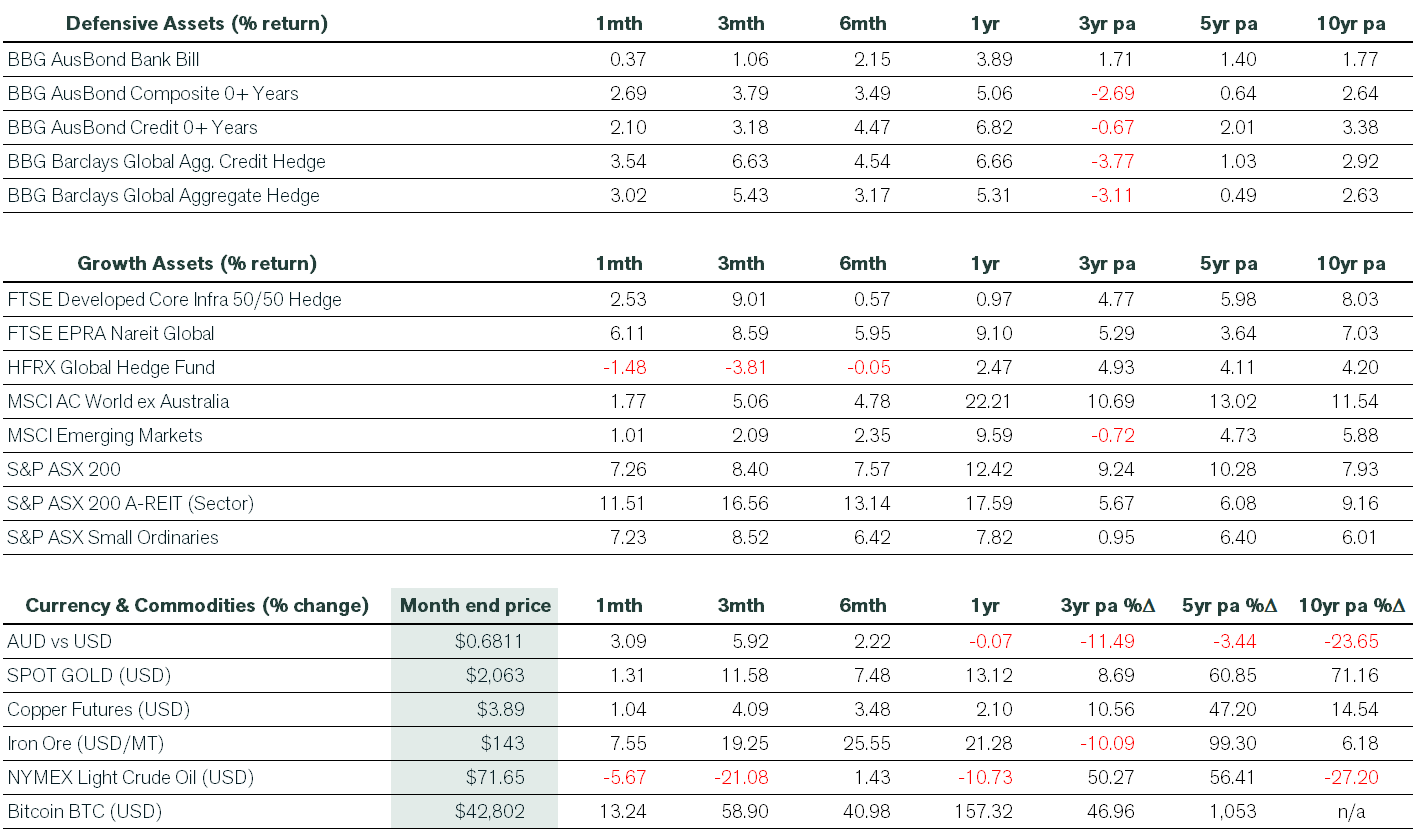

Risk-on investor sentiment continued into December as markets rallied across the major asset classes. Investors gained more confidence that the Fed was done with its rate hiking cycle and that the first of many rate reductions in 2024 could be just months away. The ‘higher for longer’ narrative that had prevailed as recently as October had given way to a more dovish outlook. Inflation data has continued to improve, and central banks are showing increasing signs that price pressures would likely continue to abate in 2024. This resulted in equities moving sharply higher into year-end, with most sectors participating in the gains.

Domestic shares were especially strong, having lagged global markets for much of 2023. Listed property and healthcare stocks staged a thumping recovery during the month, closely followed by materials (including resources) as iron ore climbed above USD 140/t. Small caps also had a strong month, with some investors adding to positions based on attractive relative valuations. Energy was the weakest performing sector, but still finished well in the black. Developed market shares rallied strongly, but the rise of the Australian dollar took the polish off returns for domestic investors. Emerging market equities underperformed their developed market peers as China continued to pose vexing questions around the structural headwinds facing its economy.

Bond markets rallied as risk-free rates moved back to levels last seen in July 2023 on hopes that global central banks would begin to cut rates in the first half of 2024. Credit markets were also strong, but different regions experienced widely varying spread outcomes due to idiosyncratic factors. The US 10-year Treasury reached 3.8% late in the month, while the yield for the domestic 10-year bond moved to as low as 3.9%. As recently as October, these instruments were yielding as much as 5%. By month’s end, money markets were positioning for six interest rate cuts in the US over the next twelve months.

Of note was the resurgence of crypto returns, with Bitcoin adding more than 13% in December in anticipation of the approval of an exchange-traded fund investing directly in the biggest token.

On the economic front, the disinflation narrative gained further momentum during the month. The US headline CPI for November slowed to 3.1% from a year ago. Falling energy prices were the main driver. Excluding volatile food and energy prices, the core CPI was up 4% from a year ago. Both numbers were in line with estimates and had little change from October. Shelter prices, which comprise about one-third of the CPI weighting, were up 6.5% on a 12-month basis, having peaked in early 2023. The December Fed meeting again kept rates on hold, but committee members now expected three rate cuts in 2024. That’s less than what the market had been pricing, but more aggressive than what officials had previously indicated. The committee’s “dot plot” of individual members’ expectations indicates another four cuts in 2025.

In Australia, the September quarter GDP numbers confirmed that a per capita recession was persisting and that the high cost of living was eating into household savings. The Australian economy expanded by 0.2% during the quarter, below market forecasts, as household consumption stalled and net trade detracted from growth. The household savings ratio dropped to 1.1%, the lowest since 2007. Meanwhile, government spending rose more quickly, preventing an overall weaker result. The unemployment rate increased to 3.9% in November 2023, while monthly inflation data pointed to slower price increases late in the year.

Elsewhere, the UK growth rate came in below consensus for October, while the German economy contracted by 0.4% year-on-year in the third quarter of 2023. Finally, in China, retail sales expanded by 10.1% year-on-year in November 2023, but below the market consensus estimate of 12.5%. Meanwhile, property prices in China posted a fifth consecutive month of decline in November, despite Beijing having issued a series of measures to boost demand.

We hope you find the information useful, and if you want to discuss any details further or discuss your personal investment strategy, please book a chat here.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).