By Pete Pennicott | May 10, 2024

By Pete Pennicott | May 10, 2024

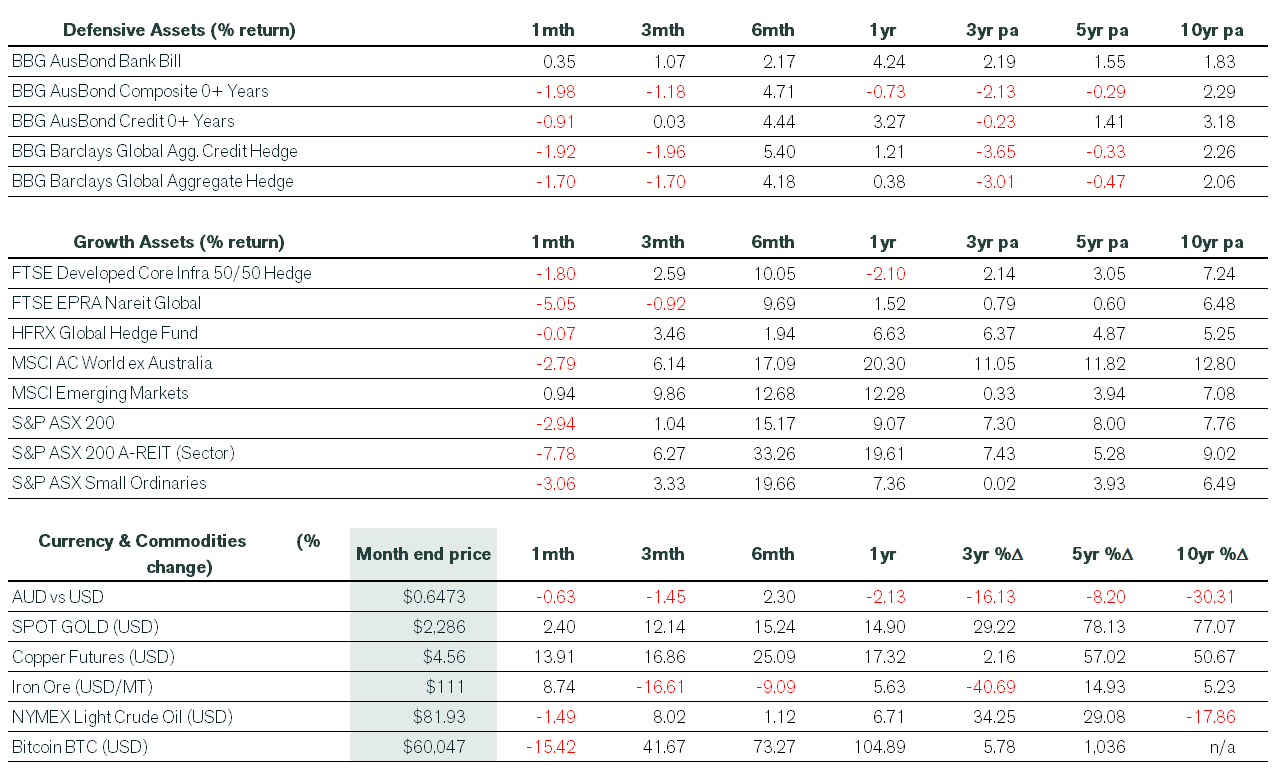

Sticky inflation data spooked markets in April, reversing much of the momentum seen in recent months. Strong US payrolls data, followed by higher-than-expected consumer and producer inflation data caught investors off guard and led money markets to unwind any positioning for a US rate cut before July. Australia was not spared from disappointing inflation data, with a higher than expected March quarter CPI result seeing markets remove all expectations of a cut to the official cash rate in 2024 and intensifying pressure on the federal government to rein in spending. The upside inflation surprises hurt both bonds and equities, with most asset classes printing negative returns in April.

In US dollar terms and after accounting for dividends, the benchmark US S&P 500 lost 4.1% in April, the Dow Jones Industrial Average lost 4.9%, while the Nasdaq lost 4.4% during the month. In broad terms, this was the first month since October that key indices printed in the red. On the domestic front, the ASX 200 accumulation index dropped 2.9% in April, slightly outperforming its small-cap peers, which fell 3.1% during the month. Following its stellar performance in March, the A-REIT sector slumped 7.8% but retained an impressive 33.3% 6-month return.

The MSCI ACWI ex-Australia index posted a loss of 2.8% in April, with unhedged domestic investors helped by a slightly weaker Australian dollar over the month. The negative news came thick and fast, as macro data continued to defy weaker expectations and geopolitical tensions reached boiling point between Israel and Iran. Iran directly launched a drone and missile attack on Israel in response to Israel’s bombing of its embassy in Syria. Israel shot down most of the missiles and later launched a focused attack of its own. Iran failed to respond and tensions quickly moderated.

While developed market equities lurched lower in April, emerging markets equities were a bright spot. In Australian dollar terms, the MSCI Emerging Markets index returned nearly 1%, helped by a modest lift in the China Shanghai Composite Stock Market Index. Higher copper and iron ore prices also boosted returns in emerging market commodity exporters. Meanwhile, the macro landscape remained supportive to corporate earnings and the US Q1 earnings season largely saw companies beat relatively low expectations. By the same token, companies that missed estimates were severely punished unless management painted a hopeful picture of the future. Tesla did precisely this – easily missing revenue expectations but announcing an exciting new initiative.

For fixed interest markets, it was a case of ‘here we go again’ as yields surged higher and credit spreads widened from relatively tight levels. In late April, the implied yield on a US 10-yr Treasury exceeded 4.7%, with the entire yield curve shifting higher throughout the month. It was a similar story in Australia, with 10-year Commonwealth government bond yields briefly exceeding 4.6%.

Meanwhile, cash, gold, copper and iron ore posted positive returns in April. In contrast, Bitcoin lost 15% but was still more than double its price from a year ago. Crude oil prices also finished slightly in the red by month’s end after tensions between Israel and Iran were ultimately restrained, as wiser heads look to have prevailed.

On the economic front, Australia’s March quarter CPI printed well above expectations across headline and underlying measures, as government-linked service items jumped. Childcare, education and pharmaceutical prices tend to reset at the start of the year and were sharply higher in 2024. Meanwhile, rents and personal services were much stronger than expected, rising by more than 2% during the quarter. The underlying measure of trimmed mean inflation rose 1% in the quarter, prompting some economists to call for a rate rise before inflation became further entrenched. The disappointing inflation print further questioned the potential impact of the upcoming Stage 3 tax cuts.

In the US, a hot CPI print came soon after strong employment and retail sales data. Nonfarm payrolls topped 300k in March and retail sales posted strong consumer spending over consecutive months. But it was the CPI that drew the most attention, rising 0.4% in March. The composition of the rise was of particular concern. ‘Supercore’ inflation is a measure of services inflation that excludes shelter and rent costs. This closely-watched measure rose by 4.8% over twelve months and has moved higher since October to be at its highest level since March 2023. Later in the month, some investors breathed a sigh of relief as March quarter US economic growth was lower than projected. However, this led more bearish market commentators to suggest that a period of ‘stagflation’ was now beginning to take shape.

Elsewhere, the Eurozone’s flash composite PMI (Purchasing Managers’ Index) rose to 51.4 in April, well above the contractionary levels seen at the end of 2023. The UK composite PMI indicated even stronger expansion. Meanwhile, Eurozone inflation in April remained at 2.4% over the year, with some signs of slowing services inflation. This increased investor confidence around the prospects for a rate cut from the European Central Bank, possibly in July, and a second rate cut by year end.

Thanks for reading. If you want to discuss your investment strategy, please book a chat here.

Pete is the Co-Founder, Principal Adviser and oversees the investment committee for Pekada. He has over 18 years of experience as a financial planner. Based in Melbourne, Pete is on a mission to help everyday Australians achieve financial independence and the lifestyle they dream of. Pete has been featured in Australian Financial Review, Money Magazine, Super Guide, Domain, American Express and Nest Egg. His qualifications include a Masters of Commerce (Financial Planning), SMSF Association SMSF Specialist Advisor™ (SSA) and Certified Investment Management Analyst® (CIMA®).